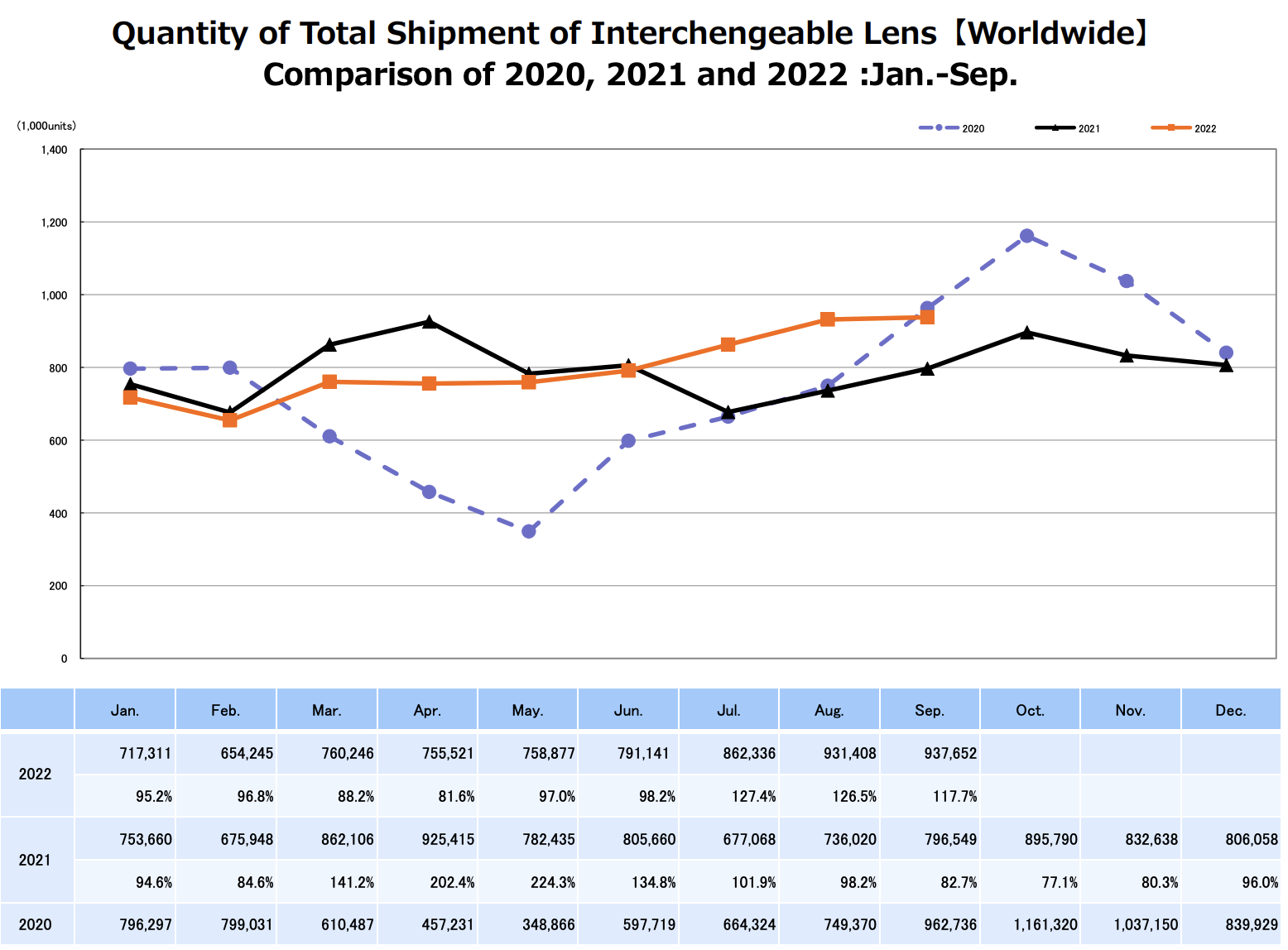

CIPA (Camera & Imaging Products Association in Japan) published their latest camera production data (orange: 2022, black: 2021, blue: 2020):

September 2022 CIPA numbers by ZoetMB

As compared with August 2022, DSLR and Compact shipments were down (but shipped value was up) and Mirrorless shipments and values were up. Lenses for smaller than 35mm sensors were up and lenses for larger sensor were down (but shipped value was up).

As compared with September 2021, DSLR shipments were up 3.8%, Mirrorless was up 54% and compacts were down 29.5%. Lenses for smaller than 35mm sensors were up 20.5% and lenses for larger sensors were up 15%.

Mirrorless bodies now take 84.9% of ILC shipped value.

CIPA has predicted 5.29 million DSLR and Mirrorless bodies for calendar 2022 and Nikon has predicted a market of 5.1 million for April ‘22 to March ‘23. We predicted 4.75 to 5.14 million units in June, 5.08 to 5.36 million units in July, 5.1 to 5.5m in August and are now predicting about 5.6 million as compared to:

2021: 5.348 million

2020: 5.308 million

2019: 8.462 million

2018: 10.76 million

2017: 11.68 million

2016: 11.61 million

2015: 13.06 million

2014: 13.84 million

2013: 17.13 million

2012: 20.16 million

2011: 15.69 million

2010: 12.89 million

2009: 9.91 million

2008: 9.7 million

2007: 8.26 million

Jan-Sep 2022 Units & Shipped Value:

(All comparisons to YTD 2021)

DSLR Units : 1.36 million –19% YTD

DSLR Shipped Value: ¥63.9 billion –7% YTD

Mirrorless Units: 2.87 million +24% YTD

Mirrorless Shipped Value: ¥358.7 billion +56% YTD

Compact Units: 1.5 million –35% YTD

Compact Shipped Value: ¥47.6 billion -13% YTD

Lenses for smaller than 35mm Units: 3.6 million –4% YTD

Lenses for smaller than 35mm Shipped Value: ¥64.2 billion +12% YTD

Lenses for 35mm and larger Units: 3.54 million +9% YTD

Lenses for 35mm and larger Shipped Value: ¥257.8 billion +41% YTD

Cumulative 2022 Mirrorless unit share (of Mirrorless + DSLR): 67.8% (was 58% YTD 2021)

Cumulative 2022 Mirrorless Shipped Value share: 84.9% (was 77% YTD 2021)

The ratio of lenses shipped to bodies shipped is 1.7 for YTD 2022. It was 1.75 for YTD 2021.

Year to Date 2022 Geographic Share:

DSLR:

Units: China 10.7%, Asia (not incl. China or Japan) 11.3%, Japan 3.9%, Europe 39.2%, Americas 33.1%, Other 1.7%

Shipped Value: China 18.6%, Asia (not incl. China or Japan) 13%, Japan 4.5%, Europe 32.2%, Americas 30.3%, Other 1.3%

Mirrorless:

Units: China 21%, Asia (not incl. China or Japan) 16.2%, Japan 9.9%, Europe 26%, Americas 23.1%, Other 3.7%

Shipped Value: China 23.3%, Asia (not incl. China or Japan) 16.4%, Japan 8.9%, Europe 22.4%, Americas 24.7%, Other 4.4%

Compacts:

Units: China 9.5%, Asia (not incl. China or Japan) 12%, Japan 23.6%, Europe 29.4%, Americas 21.4%, Other 4.1%

Shipped Value: China 13.9%, Asia (not incl. China or Japan) 13.6%, Japan 17%, Europe 28.6%, Americas 23.4%, Other 3.4%

Lenses:

Units: China 15.3%, Asia (not incl. China or Japan) 13.3%, Japan 9%, Europe 31.6%, Americas 27.5%, Other 3.4%

Shipped Value: China 18.7%, Asia (not incl. China or Japan) 13.6%, Japan 9.7%, Europe 26.9%, Americas 26.9%, Other 4.3%

{kind=link}